SMM, June 4:

Today, spot primary aluminum prices rebounded by 160 yuan/mt from the previous trading day. SMM A00 aluminum ingot prices closed at 20,280 yuan/mt, with aluminum scrap market prices adjusting unevenly. As the off-season begins in June, downstream scrap utilisation enterprises are experiencing weak order releases, with procurement mainly driven by immediate needs.

Today, the centralized quotes for baled UBC aluminum scrap range from 15,100 to 15,600 yuan/mt (tax excluded), while the centralized quotes for shredded aluminum tense scrap range from 15,500 to 17,000 yuan/mt (tax excluded). Regionally, Shanghai, Jiangsu, Henan, Shandong, Guizhou, and other regions closely track aluminum prices, with price adjustments ranging from 100 to 150 yuan/mt. In Jiangxi and Foshan, price adjustments lag behind aluminum prices, with quotes remaining unchanged from yesterday. By product, the overall prices of baled UBC aluminum scrap have rebounded, with single-day adjustments of 100 yuan/mt in Sichuan, Chongqing, Shanghai, Zhejiang, and other regions, while Jiangxi and Foshan have chosen to maintain their prices. For shredded aluminum tense scrap, the overall quotes have rebounded by 100-150 yuan/mt.

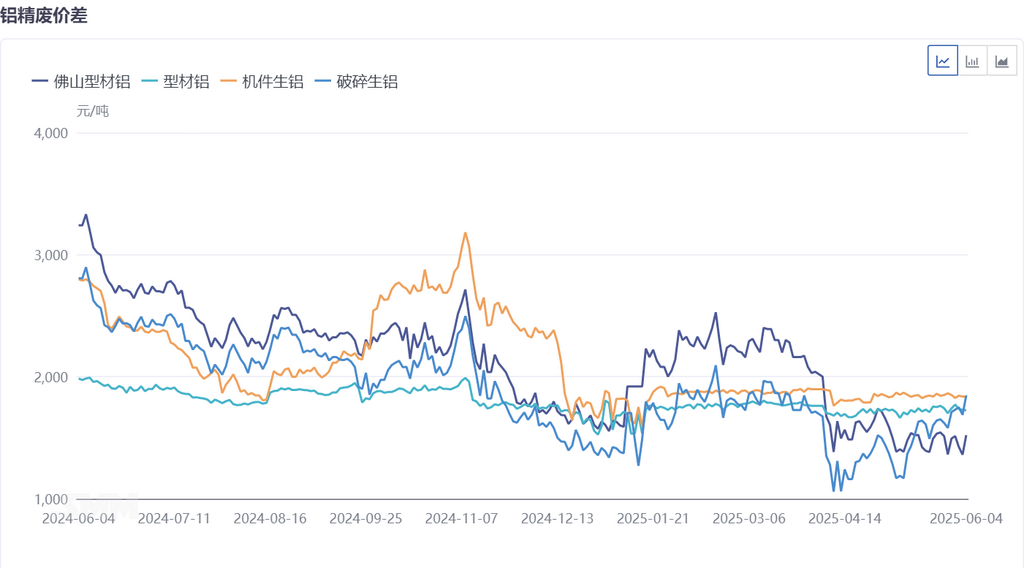

In terms of the price difference between A00 aluminum and aluminum scrap, the price difference between A00 aluminum and mechanical casting aluminum scrap in Shanghai decreased by 10 yuan/mt from last Friday, narrowing to 1,835 yuan/mt. The price difference between A00 aluminum and aluminum extrusion scrap in Foshan increased by 100 yuan/mt from last Friday to 1,522 yuan/mt.

In the short term, aluminum scrap market prices are expected to continue fluctuating at highs. The tight supply situation for aluminum tense scrap is unlikely to change, providing solid price support. Wrought aluminum alloy scrap will continue to fluctuate rangebound with primary aluminum, but the cumulative risk of high-level corrections in primary aluminum, combined with weak demand during the off-season, will limit upside room. For downstream scrap utilisation enterprises, cost pressure and weak terminal orders continue to compete, with operating rates likely to remain low. Narrowing import losses may partially alleviate supply pressure, but the transmission effect will be limited. Regional and product price differences may further diverge, with tight supplies in South China and other regions potentially supporting localized price increases, while prices in regions with weak demand will face downward pressure.